XRPL Lending: The Missing DeFi Primitive for a ~$66B Asset

XRPL’s lending layer is designed for credit, not just DeFi yield

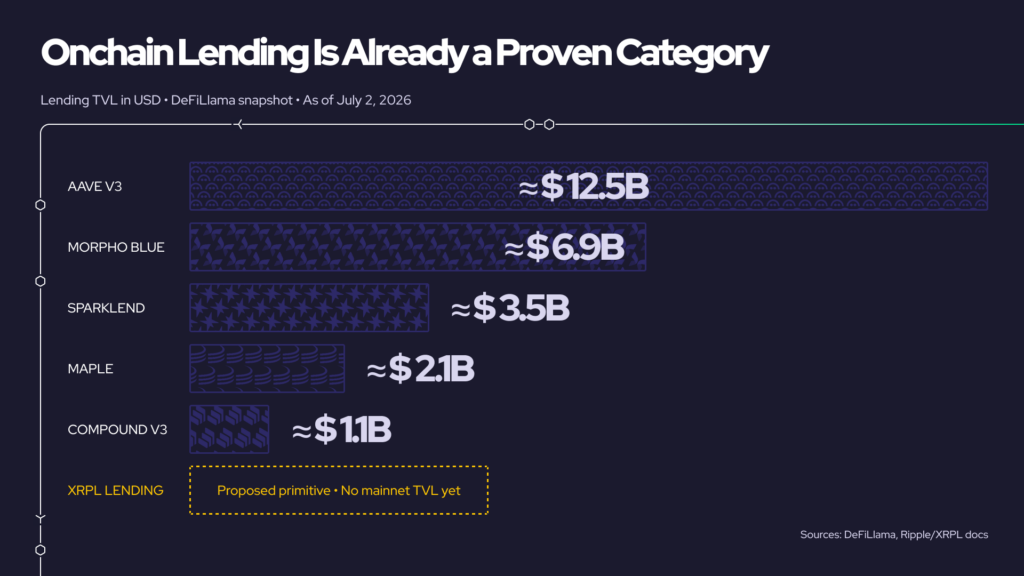

The Lending Category Was Already Proven

DeFi users do not need to be convinced that lending matters. Aave, Morpho, SparkLend, Compound, Maple and other protocols have already shown that onchain credit can attract deposits, create steady borrowing demand and generate meaningful fees. Aave V3 alone sits in the $10B+ TVL range, while Maple shows that underwritten credit can also work onchain for institutional borrowers.

The question is not whether lending is a valuable DeFi category; that part is settled. The question is what happens when XRPL, a network with a large native asset but a still-thin DeFi layer, starts building a lending layer of its own.

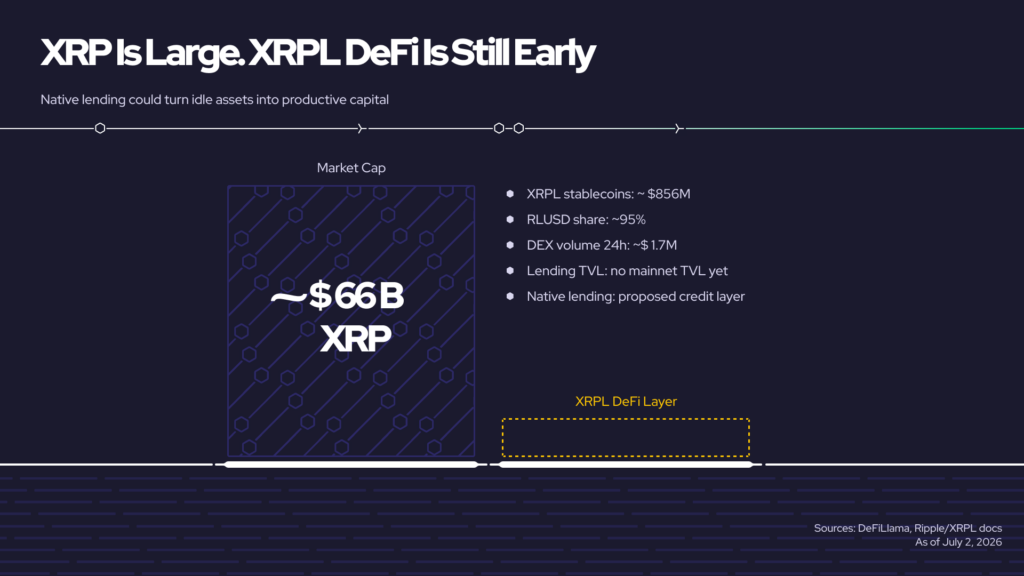

XRP already trades like a major asset, with a market cap around $66B and deep liquidity across platforms. XRPL, however, does not yet have a lending market comparable to Aave, Morpho, Maple or Compound. That gap is the core thesis: XRP is large, XRPL DeFi is early, and lending is one of the most obvious missing pieces.

What XRPL Lending Actually Is

Ripple published the XRPL Lending Protocol design on June 29, 2026. The design is built around two proposed amendments: XLS-65, or Single Asset Vault, and XLS-66, the Lending Protocol. Together, they define a native credit layer for XRPL rather than a standalone app or frontend.

A Single Asset Vault pools one asset type. Depositors provide liquidity, while the vault handles accounting for deposits, withdrawals, shares and losses. The Lending Protocol connects those vaults to fixed-term loans with defined conditions: interest, repayment logic, grace periods, default handling and first-loss capital.

The key design choice is the split between offchain underwriting and onchain execution. XRPL is not trying to decide whether a borrower is creditworthy; that still depends on institutional risk processes, compliance, documents and borrower relationships. The protocol’s role is to make the agreed loan lifecycle transparent, enforceable and auditable once the credit decision has been made.

XRPL is entering a proven lending category before it has live lending traction.

Not Another Aave

XRPL Lending should not be described as “Aave on XRPL.” Aave and Compound are collateral-first systems: users deposit collateral, borrow against it, and risk is managed through LTVs, price oracles, liquidations and overcollateralization. That model works because crypto-native collateral is liquid and constantly priced.

XRPL Lending is closer to Maple or Clearpool. Borrowers are known, credit quality matters, and underwriting cannot be reduced to a liquidation threshold. The protocol does not replace the credit decision; it enforces the credit agreement once that decision has been made.

That distinction matters for XRPL’s likely user base. Payment companies, market makers, treasury desks, tokenized asset issuers and regulated lenders are more likely to need predictable credit lines than anonymous leverage trades. XRPL already has a payments and settlement narrative, RLUSD, tokenized asset ambitions and infrastructure for permissioned access. Lending adds the missing credit layer to that stack.

XRP is already a major asset while XRPL’s lending market is still mostly unbuilt.

Why This Matters for XRP

This is not a fee-burn argument or a claim that TVL will arrive immediately. The stronger argument is expanded utility. XRP is mostly understood through payments, settlement, liquidity and institutional transfer use cases. Lending could add another layer: putting idle assets to work.

The honest part: XRPL Lending is not live at scale on mainnet yet. XLS-65 and XLS-66 still require validator approval, and devnet testing is not the same as adoption. The metrics that will matter later are vault deposits, active loan volume, repayments, defaults and integrations with payment or tokenized asset infrastructure.

If XRPL can turn XRP, RLUSD and tokenized assets into productive capital, XRP’s role could expand beyond payments and settlement into onchain credit and capital markets. That makes XRP the simplest asset to watch for users following XRPL’s move into lending.

A DeFi Route Into XRP

For users looking for a DeFi-native way to access XRP, Rubic aggregates XRP routes across up to 7 competing providers, with more to come. That means you can compare available options for the best available rate and timing instead of relying on one provider.

If XRPL is moving toward a native credit layer, XRP is the most direct asset tied to that shift. Rubic makes that access easier.

Rubic lets users compare XRP routes across providers before swapping

Content Lead at Rubic with a deep dive into Web3 trends, industry narratives, and market analysis